Out with the Old and In with the New Financial Reporting Standards for Nonprofits

By John D'Amico | October 2, 2018

It has now been twenty-five years since the Financial Accounting Standards Board (FASB) issued Statement of Financial Accounting Standards (SFAS) No. 117, Financial Statements for Not-for-Profit Organizations. At the time, this standard introduced significant changes to the way nonprofits reported their financial results by requiring them to report by net asset classes rather than fund accounting.

Though the SFAS 117 financial reporting model has been used by all nonprofits since its release, it has lately become evident that improvements were needed for the current net asset classifications, the liquidity and availability of resources, inconsistencies in financial reporting and better comparability among nonprofit organizations. As a result, FASB has issued Accounting Standards Update (ASU) 2016-14, Presentation of Financial Statements of Not-for-Profit Entities, to address these areas.

These new financial reporting standards take effect for all nonprofits with fiscal year-ends of December 31, 2018 and thereafter. The amendments in this update should be applied on a retrospective basis in the year that the update is first applied.

IMPROVEMENTS TO THE NET ASSET CLASSIFICATIONS

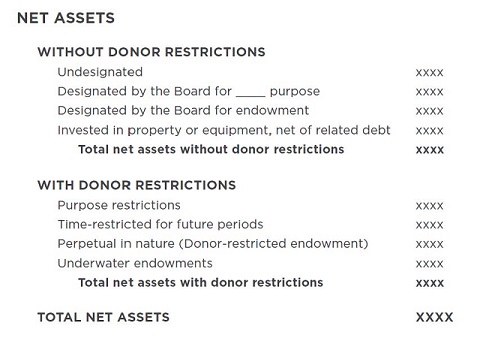

A key change to the financial statements of nonprofits found in ASU 2016-14 is the overall improvement and clarification of the descriptions of the three net asset classes: unrestricted, temporarily restricted, and permanently restricted net assets. In the past, the meaning of unrestricted net assets was often misinterpreted. Though unrestricted net assets meant only that there were no donor restrictions, potential legal restrictions or internally designated board restrictions within the unrestricted net assets would result in the net assets not being available to meet obligations. To combat the confusion, FASB now requires that net assets be classified as either net assets with donor restrictions or net assets without donor restrictions.

Net assets with donor restrictions will now include both the temporarily restricted and permanently restricted net assets. This change was much needed following the issuance of the Uniform Prudent Management of Institutional Funds Act (UPMIFA), which allowed nonprofits to prudently spend the principal of their permanently restricted net assets, therefore no longer permanently restricting the assets.

To enhance the information regarding net assets without donor restrictions, the ASU will require nonprofits to disclose the amounts and purposes of governing board designations that result in self-imposed limits on the use of resources at the end of their reporting period. This can be accomplished by showing the board-designated amount as a component of the net assets without donor restrictions on the statement of financial position and a footnote describing the purposes for these resources.

Although not required, nonprofits with a significant amount of “brick and mortar” that is not available to meet current obligations should consider adding another component (net investments in property and equipment) to their net assets without donor restrictions.

While some nonprofits may not have all of these categories within their net assets, here is an example of how the net asset section on the statement of financial position can look:

The level of detail presented above is not required. However, if the information presented on the face of the financial statement is not sufficiently detailed, it must be included in the footnotes.

IMPROVEMENTS TO INFORMATION ABOUT LIQUIDITY AND AVAILABILITY OF RESOURCES

Liquidity refers to how easily assets can be converted to cash and be made available to meet current liabilities. Therefore, cash is the most liquid asset, followed by short-term operating investments and receivables.

Currently, Generally Accepted Accounting Principles (GAAP) require that assets be listed on the balance sheet in order of liquidity. This is all that nonprofits (or businesses) are required to disclose about the liquidity of their assets. FASB’s ASU 2016-14, however, will now require that all nonprofits disclose quantitative information about their financial assets at the balance sheet date to meet cash needs for general expenditures within one year of the balance sheet date.

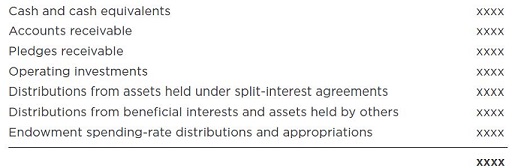

This should be addressed in a new footnote entitled Liquidity and Availability. This footnote should list all financial assets that are not associated with donor, internal or legal restrictions that are available for general expenditures. Financial assets are cash or cash equivalents, operating instruments and receivables. An example of this footnote is as follows:

NOTE X – LIQUIDITY AND AVAILABILITY

Financial assets for general expenditures that are without donor, internal or other restrictions limiting their use, within one year of the balance sheet date, comprise the following:

Qualitative information communicating how a nonprofit manages the liquid resources available to meet cash needs for expenditures within one year of the balance sheet date will also be required.

CONSISTENCY FOR COMPARABILITY PURPOSES AMONG NONPROFITS

When SFAS 117 was written, it was believed that a significant amount of flexibility was needed for nonprofit financial reporting due to the many different types of nonprofits. However, because of the flexibility in financial reporting that was allowed, it has been difficult to compare financial performance between nonprofits, even of the same type. FASB’s ASU 2016-14 is intended to introduce consistency, which will enhance comparability among nonprofits in the following areas: reporting of expenses, reporting of investment income and expirations of restrictions on gifts of long-lived assets.

REPORTING OF EXPENSES

Currently, all nonprofits are only required to report their expenses by functional category — that is, by Program, Management & General and Fundraising. (Nonprofits which meet the criteria for a Voluntary Health and Welfare Organization must report their expenses by both functional and natural classifications.)

FASB’s ASU 2016-14 will now require that all nonprofits report their expenses in one place by both functional and natural classifications. This can be done on the statement of activities, in the footnotes, or in a separate statement such as a statement of functional expenses. Presenting this information as supplementary information does not meet this requirement.

REPORTING OF INVESTMENT RETURN

At present, nonprofits can disclose their investment return net of investment management fees paid to an investment advisor. For some nonprofits, however, the investment portfolio is managed internally by their Chief Financial Officer or Executive Director. To improve consistency moving forward, FASB’s ASU 2016-14 will now require that a nonprofit’s investment return be shown net of both external and direct internal investment expenses. The internal investment expenses are limited to a portion of the person’s salary and related salary expenses, allocated based on their estimated time to manage the investment portfolio.

Disclosing the components of investment return such as realized/unrealized capital gains and interest and dividends is no longer needed. External investment expenses also no longer need to be disclosed. Only the direct internal investment expenses, if any, need to be disclosed.

EXPIRATIONS OF RESTRICTIONS ON GIFTS OF LONG-LIVED ASSETS

In cases where there isn’t an explicit donor restriction, nonprofits currently have the option to impose a time restriction on gifts of long-lived assets and record the gift as temporarily restricted. This enables the non- profit to offset the depreciation expense over the estimated useful life of the asset with a release from temporarily restricted net assets, and thus has no effect on the unrestricted net assets over the remaining life of the long-lived asset. However, not all nonprofits took advantage of this option, which created inconsistencies among nonprofits that received gifts of long-lived assets.

FASB's ASU 2016-14 will no longer allow nonprofits to impose a time restriction, and instead requires that nonprofits use the placed-in-service approach on all gifts of long-lived assets. In addition, nonprofits must reclassify any remaining amounts from net assets with donor restrictions to net assets without donor restrictions as of the beginning of the period of adoption of ASU 2016-14.

OTHER CHANGES AS REQUIRED BY FASB’S ASU 2016-14 OPERATING CASH FLOWS

FASB’s ASU 2016-14 will continue to allow nonprofits to present their operating cash flows using either the direct or indirect method. To encourage use of the direct method, nonprofits will no longer need to present the reconciliation to the indirect method.

UNDERWATER ENDOWMENTS

An underwater endowment is a donor-restricted endowment for which the fair value of the fund at the reporting date is less than either the original gift amount or the amount required to be maintained by the donor or by law that extends donor restrictions. Until now, underwater endowments were recorded within the unrestricted net assets. FASB’s ASU 2016-14 will require underwater endowments to be reported within net assets with donor restrictions.

ALLOCATING COSTS AMONG PROGRAM AND SUPPORTING FUNCTIONS

Nonprofits will now be required to provide an enhanced qualitative description of the method(s) used to allocate costs among program and support functions. The following is an example from FASB’s Codification guidance:

The financial statements report certain categories of expenses that are attributable to one or more programs or supporting functions of the Organization. Those expenses include depreciation and amortization, the president’s office, communications department, and information technology department. Depreciation is allocated based on square footage, the president’s office is allocated based on estimates of time and effort, certain costs of the communications department are allocated based on estimates of time and effort, and the information technology department is allocated based on estimates of time and costs of specific technology utilized.

CONCLUSION

By consolidating and clarifying net asset classes, improving consistency and enhancing the disclosures that lenders, bondholders, donors and grantors use in their decision-making processes, the changes required by FASB’s ASU 2016-14 will enable nonprofits to better tell their financial stories.

About John D'Amico

John D'Amico, CPA, is a Partner within the Professional Standards Group at Marks Paneth LLP, which is responsible for monitoring quality control in the firm as mandated by professional standards. He specializes in pre-issuance reviews and inspections of nonprofit organizations, governments and Single Audits. Mr. D’Amico also provides consultation on accounting and attestation matters and tests and monitors the firm's quality review policies and procedures. He teaches continuing education classes for the firm and on... READ MORE +